Table of contents

ToggleIntroduction

Private credit has quietly grown into a 1.7 trillion dollar powerhouse, yet most retail investors still overlook it. In a world shaped by aggressive monetary tightening and shrinking bank balance sheets, this shadow giant is becoming the new engine of global lending. What was once a niche corner of the financial markets now stands at the center of global capital allocation, attracting institutions, sovereign funds, and ultra high net worth investors who are searching for resilient yield.

The rise of private credit is not a simple trend driven by market cycles. It is the result of long term structural forces that have reshaped the relationship between borrowers and lenders since the Global Financial Crisis. As traditional banks tighten lending standards and regulators impose stricter rules, non bank lenders are stepping in to fill the gap. Their speed, flexibility, and bespoke financing solutions are transforming how companies fund their growth, especially in the mid market segment.

At the same time, the current high rate environment has created ideal conditions for private credit to thrive. Floating rate structures, wider spreads, and stronger lender protections have positioned the asset class as one of the most attractive sources of yield available today. Yet behind the impressive returns lies a complex world that demands a clear understanding of risk, liquidity constraints, and the evolving competitive landscape.

This article explores why private credit is emerging as the new king of yield, how its rapid expansion is changing modern finance, and what investors need to consider before entering one of the fastest growing asset classes of the decade.

I. The Rise of Private Credit in Today’s Financial Landscape

1.1 A Historical Shift in Global Lending

Private credit did not emerge overnight. Its rise reflects a gradual but powerful realignment of global lending that began in the aftermath of the 2008 financial crisis. For decades, banks dominated corporate financing. They controlled the flow of credit, shaped lending standards, and operated with relatively few competitors outside the public bond markets. The crisis fundamentally changed this balance. Governments and regulators responded with stricter capital requirements, tighter leverage rules, and more demanding stress tests. These measures were designed to stabilize the financial system, but they also constrained the ability of banks to lend freely, particularly to mid sized and highly leveraged companies.

This regulatory shift created a vacuum. Companies still needed capital to expand, acquire competitors, or manage liquidity pressures, yet banks became less willing to hold certain types of loans on their balance sheets. Investors, on the other hand, were facing an environment defined by near zero interest rates and shrinking yields across traditional fixed income. The combination of strong demand for capital and a global search for income opened the door for private lenders who were not subject to the same regulatory constraints.

Private credit funds stepped into this space with determination. At first, they focused mainly on middle market direct lending, offering loans to businesses that struggled to obtain financing from banks. Over time, the scope broadened. Private lenders began financing larger companies, participating in leveraged buyouts, and even providing specialty financing in areas such as real estate, infrastructure, and asset backed lending. What began as a niche strategy became a central pillar of modern corporate finance. The private credit market expanded rapidly, fueled by institutional investors seeking higher returns and by private equity firms eager to pair their acquisition strategies with flexible lending partners.

The result is a profound historical shift. The flow of capital is no longer dominated by the banking system. A parallel credit ecosystem now exists, and it continues to grow at a pace that rivals any other segment of the global financial markets.

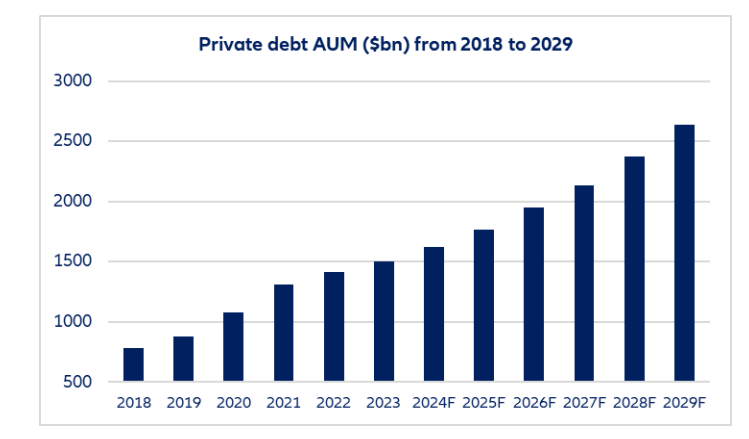

Private credit has experienced a dramatic expansion over the past decade, driven by tighter banking regulations, growing institutional demand for yield, and the increasing role of private markets in corporate financing. As the chart shows, global private debt assets have grown steadily from 2018 onward and are projected to surpass 2.5 trillion dollars by 2029. This sustained rise highlights the structural shift taking place in global lending and sets the foundation for the asset class to play an even more central role in the years ahead.

1.2 Understanding What Makes Private Credit Unique

To understand why private credit has become so influential, it is important to grasp what differentiates it from its public market counterparts. Private credit refers to lending that takes place outside of traditional banks or public bond markets. Loans are negotiated directly between a lender and a borrower. Because these transactions are private, they can be personalized to meet the specific needs of the company. This flexibility is one of the greatest advantages of the asset class.

Unlike public bonds, private credit does not require issuers to go through ratings agencies or comply with extensive disclosure requirements. Borrowers appreciate the confidentiality and the faster decision making process. Lenders value the ability to structure deals with strong covenants, seniority protections, and collateral packages that reduce risk.

Another defining characteristic is illiquidity. Investors in private credit accept that their capital will be locked up for years. In exchange, they receive higher yields than what is typically available in public debt markets. This illiquidity premium is one of the main drivers of performance. The lack of daily market pricing also means portfolios are less exposed to short term volatility, which many institutional investors consider a benefit.

Private credit also differs from high yield bonds and leveraged loans. While these public market instruments involve large syndicates of investors and standardized terms, private credit is more concentrated. A single fund or a small group of lenders may provide the entire loan, which allows for deeper due diligence and stronger governance oversight. The relationship between borrower and lender is closer and more long term, making it easier to negotiate amendments or extensions when a company faces difficulties.

These distinctive features have allowed private credit to carve out a position that blends attractive returns with risk management mechanisms that appeal to sophisticated investors. It operates in a space that is too rigid for banks and too customized for public markets, which explains its rapid ascent.

1.3 The High Rate Environment: A Catalyst for Growth

The current macroeconomic environment has propelled private credit to new heights. Over the past two years, central banks around the world have engaged in the most aggressive tightening cycle in decades. Interest rates have risen sharply in response to persistent inflation and continued economic uncertainty. While higher rates have pressured traditional bond markets, they have strengthened private credit, particularly direct lending.

One key reason is the prevalence of floating rate structures. In most private credit deals, interest payments adjust automatically as benchmark rates increase. This means that lenders benefit directly from rising rates. At a time when many fixed income portfolios have suffered losses due to falling bond prices, private credit investors have seen their yields climb to levels that were not available for more than fifteen years.

Borrowers accept these higher costs because private lenders offer something banks often cannot: speed, certainty, and customization. In periods of elevated rates, companies face greater refinancing pressures. They cannot afford lengthy processes or sudden shifts in bank lending criteria. Private lenders provide faster commitments and the ability to negotiate terms based on the borrower’s strategic needs rather than rigid underwriting formulas.

The high rate environment also makes private credit more competitive relative to other investment strategies. Equity markets remain volatile, and traditional fixed income still faces duration risk. Private credit, by contrast, delivers income with shorter duration exposure and stronger covenants. Investors who seek stability in unpredictable markets find this combination compelling.

Finally, macroeconomic uncertainty has reinforced the importance of private lenders in the real economy. Many mid sized companies rely on direct lending to refinance debt, fund acquisitions, or manage working capital. As banks tighten standards, private lenders become essential partners. Their role becomes even more prominent when economic conditions slow, because companies need flexible financing to weather temporary challenges.

The convergence of these factors explains why private credit has gained prominence in today’s financial landscape. It offers yield, protection, adaptability, and relevance across market cycles. This combination positions it at the forefront of modern lending and sets the stage for its continued expansion.

II. Private Credit as the New King of Yield

2.1 A Yield Premium That Attracts Global Investors

The appeal of private credit begins with its yield premium. In the current environment, where traditional fixed income instruments often provide returns that barely outpace inflation, private credit stands out as one of the few asset classes capable of generating high single digit or even double digit annual yields. This premium is not the result of excessive leverage or speculative behavior. Instead, it reflects structural characteristics of the private lending model.

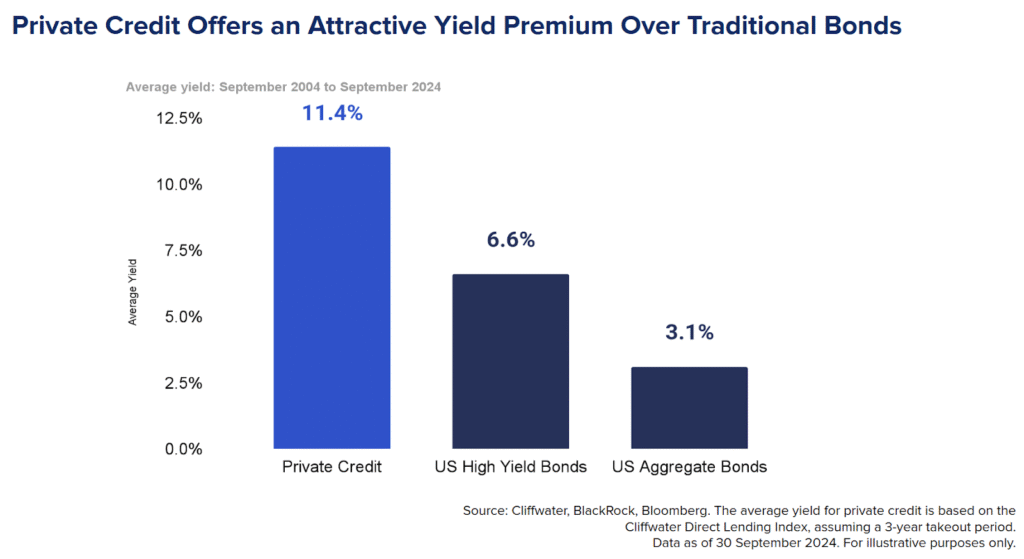

Private credit consistently delivers a yield premium that surpasses traditional fixed income categories. As the chart shows, average yields over the last two decades were more than 11 percent for private credit, compared to 6.6 percent for US high yield bonds and 3.1 percent for US aggregate bonds. This performance gap highlights why institutional investors view private credit as one of the most attractive sources of income in a high rate environment.

One of the primary sources of this premium is the illiquidity that investors accept when committing capital to private credit funds. Since these loans are not traded on public markets, investors must agree to lock up their capital for several years. This lack of liquidity creates an opportunity for higher compensation. Institutions that are less sensitive to liquidity needs, such as pension funds, insurance companies, and sovereign wealth funds, view this premium as an efficient way to enhance long term returns.

Another driver of the yield premium is the ability of private lenders to negotiate stronger terms than those available in public markets. This includes covenants that protect the lender, collateral packages, and seniority in the capital structure. These protections help reduce credit risk, yet the yields remain significantly higher than comparable public bonds.

Recent reports from firms such as Blackstone and Apollo highlight the strength of the asset class. Their flagship direct lending funds consistently report yields that exceed public high yield indices, even after accounting for fees and risk management costs. The combination of higher yields, differentiated deal structures, and stable performance through varying market cycles has strengthened the perception of private credit as a reliable income generator.

As more investors seek alternatives to volatile equity markets and low yielding bonds, private credit has positioned itself as a core allocation in institutional portfolios. The inflows reflect not only the desire for yield, but also the growing confidence in the resilience and maturity of the asset class.

2.2 The Corporate Borrowers’ Perspective

The rapid expansion of private credit is not driven solely by investor demand. Borrowers have also embraced private lenders as strategic partners in their operations and growth plans. This is particularly true for mid market companies, which often face challenges when seeking financing from traditional banks.

One major advantage of private credit is speed. Unlike banks, which must navigate layers of internal approvals and regulatory constraints, private lenders can move quickly. Decisions can be made within weeks rather than months. For companies facing acquisition deadlines, refinancing pressures, or time sensitive opportunities, this speed can be invaluable.

Another significant benefit is flexibility. Private lenders are not bound by the standardized loan structures that define traditional bank lending. They can tailor loan terms to the specific needs of the business, which may involve customized amortization schedules, creative collateral arrangements, or covenant packages designed to align incentives rather than constrain operations.

This flexibility is particularly important in leveraged buyouts. Private equity firms rely on dependable financing partners to complete transactions, and private credit funds have become essential contributors to these deals. They offer certainty of execution, a close working relationship, and the ability to provide both senior and subordinated debt within a single, coordinated structure. This allows private equity sponsors to negotiate deals with greater confidence and clarity.

Borrowers also value the relationship driven approach of private lenders. Since a small group of investors often provides a large portion of the financing, ongoing collaboration becomes easier. Amendments, extensions, or covenant adjustments can be negotiated directly rather than through a broad syndicate of investors with competing interests. This collaborative approach can make a significant difference when companies face challenging economic conditions or unexpected disruptions.

For many corporate borrowers, private credit represents not only an alternative to banks, but a more strategic and responsive financing solution that adapts to their specific needs.

2.3 Case Studies and Market Evidence

The claim that private credit is becoming the new king of yield is supported not only by theoretical advantages, but also by concrete market evidence. In recent years, numerous case studies have illustrated how private lenders have reshaped the financing landscape for companies of various sizes and sectors.

Data providers such as Preqin and PitchBook have documented steady growth in deal volumes, fundraising, and returns. Their analyses show that private direct lending funds have outperformed many categories of public fixed income on a risk adjusted basis. For example, in periods when public credit markets experienced significant volatility, private direct lending portfolios often maintained stable valuations and continued to deliver strong cash yields.

One notable example is the increasing reliance on private credit for large scale buyouts. Historically, massive leveraged buyouts were financed almost exclusively through syndicated loans and high yield bonds. In recent years, private credit funds have begun to participate in, and even lead, financing packages for multibillion dollar deals. This demonstrates not only the scale of these funds, but also their growing credibility among major financial sponsors.

The real estate and infrastructure sectors also offer compelling illustrations. Private lenders have stepped in to provide construction financing, bridge loans, and project development capital in situations where banks have pulled back due to higher capital requirements. Their involvement has supported projects ranging from commercial developments to renewable energy installations. These transactions highlight the adaptability of private credit and its ability to serve a broad range of industries.

Market evidence further shows that private credit has maintained strong performance even during periods of economic uncertainty. Although defaults have risen slightly in some segments, recovery rates remain relatively high due to strong covenant structures and collateral protections. Investors who prioritize income generation continue to view private credit as a valuable component of a diversified portfolio.

The combination of strong returns, flexible structures, and real world impact has solidified the position of private credit as one of the most attractive yield generating asset classes available today. Its rapid ascent is not a temporary phenomenon, but a reflection of deeper shifts in global finance that continue to shape the market.

III. Risks, Opportunities, and the Future of Private Credit

3.1 The Main Risks Investors Must Recognize

Despite its strong performance and rapid growth, private credit is not without significant risks. Investors who treat it as a simple substitute for traditional fixed income may underestimate the complexities involved. Understanding these risks is essential for making informed decisions in an asset class that blends opportunity with structural uncertainty.

Credit risk remains the most visible challenge. As economic conditions tighten and borrowing costs rise, some companies may struggle to meet interest payments or refinance existing debt. Private credit has historically focused on mid market companies that do not have the same financial resilience or access to capital markets as large corporations. If economic growth slows, default rates may increase. Although strong covenant structures help mitigate losses, they cannot eliminate the inherent vulnerability of lending to smaller or highly leveraged businesses.

Illiquidity risk is another critical concern. Investors who commit capital to private credit funds often face multi year lockups. Unlike public bonds, these positions cannot be easily sold, and valuation updates occur less frequently. In a period of market stress, investors may find themselves unable to exit their investments or adjust their exposure. This illiquidity is a key driver of the yield premium, but it also limits flexibility and requires careful portfolio planning.

Valuation opacity also deserves attention. Private credit portfolios do not benefit from transparent market pricing. Valuations are model driven and based on assumptions that may not fully reflect rapid changes in economic conditions. During volatile periods, this can lead to discrepancies between reported values and actual risk. Analysts from the Financial Stability Board have warned that the growing scale of the private lending market, combined with opaque pricing, may create blind spots in the global financial system.

Regulatory risk adds another layer of complexity. As private credit becomes more influential, regulators are increasingly concerned about potential systemic vulnerabilities. Although private lenders played a stabilizing role during some recent market disruptions, the rapid expansion of the sector may attract more scrutiny. Future regulation could increase compliance obligations or alter the competitive dynamics between banks and non bank lenders.

These risks highlight the need for thoughtful due diligence. Investors who approach private credit with a long term horizon and a clear understanding of its constraints can still benefit from its strengths, but they must accept that the asset class requires patience, discipline, and robust risk management.

3.2 A Promising but More Competitive Future

While risks exist, the future of private credit remains promising. The asset class continues to attract unprecedented levels of institutional capital, and new strategies are emerging that expand its reach beyond traditional direct lending. However, this growth is accompanied by intensifying competition that may reshape the landscape.

One of the most significant developments is the entrance of major global asset managers who seek to scale their private credit platforms. Firms such as Blackstone, KKR, and Apollo have raised multi billion dollar funds dedicated to direct lending, opportunistic credit, and specialty finance. Their size allows them to participate in larger deals, attract top talent, and invest in advanced data systems that improve underwriting accuracy. This consolidation strengthens the credibility of private credit, but it also means smaller managers may struggle to differentiate themselves.

The competitive environment is also driving innovation. NAV based lending, which uses the net asset value of a private equity fund as collateral, has gained popularity among sponsors seeking flexible financing solutions. Opportunistic credit strategies provide capital to companies in distress or transition, offering higher returns in exchange for greater complexity. Specialty finance, including consumer credit, equipment leasing, and asset backed lending, has expanded the universe of opportunities available to private lenders.

Although competition may compress yields over time, it can also improve the overall health of the market. Larger and more sophisticated players typically maintain rigorous underwriting standards, while increased transparency and data availability reduce information asymmetry. This maturation process suggests that private credit is evolving into a long term fixture of global finance rather than a temporary response to post crisis regulation.

Borrower demand also supports continued growth. As banks remain selective in their lending practices, companies increasingly view private lenders as strategic partners capable of supporting acquisitions, expansions, and refinancing needs. The ability of private lenders to structure tailored solutions ensures ongoing relevance, even if competitive pressures reshape pricing dynamics.

The outlook is therefore mixed but constructive. Yields may decrease gradually as capital flows accelerate, but the combination of expanding strategies, stable demand, and institutional adoption positions private credit as a durable and influential asset class.

3.3 Long Term Outlook and Structural Drivers

Looking ahead, several structural forces suggest that private credit will continue to grow over the next decade. These drivers are not tied to short term monetary policy or cyclical market movements. They reflect deeper changes in demographics, regulation, technology, and global capital allocation.

An important long term driver is the rising importance of income focused investment strategies. Ageing populations in Europe, North America, and parts of Asia are increasing demand for long horizon assets that deliver stable cash flows. Pension funds and insurance companies, which manage trillions in long term liabilities, find private credit attractive because it offers predictable income combined with lower mark to market volatility. Research by McKinsey notes that private markets, and private credit in particular, are becoming central components of institutional portfolios due to these demographic trends.

Another structural driver is the continued retrenchment of traditional banks from certain segments of the lending market. Regulatory requirements introduced after the financial crisis remain firmly in place, and recent discussions within global regulatory bodies suggest that capital buffers may increase rather than decrease. This means banks are likely to remain cautious, especially when lending to riskier or smaller borrowers. Private credit fills this gap and is becoming embedded in the functioning of modern corporate finance.

Technology will also shape the next chapter of private credit. Data driven underwriting, advanced analytics, and artificial intelligence are already improving the ability of lenders to assess risk, price loans, and monitor portfolio companies. Large asset managers are investing heavily in proprietary platforms that integrate real time financial data, supply chain metrics, and industry benchmarks. This technological shift enhances efficiency and provides a competitive advantage that sets private lenders apart from traditional financial institutions.

Finally, the globalization of private credit is accelerating. Markets in Europe and Asia are experiencing rapid growth as companies seek alternatives to traditional lending channels. Cross border private lending is becoming more common, supported by increasing investor interest from regions such as the Middle East. As the ecosystem expands geographically, it becomes more diversified and less dependent on economic conditions in any single region.

These long term drivers suggest that private credit is not simply riding the wave of a high rate environment. It is becoming a permanent and influential component of global finance. Its future will involve a balance between opportunity and discipline, innovation and risk management, growth and regulation. Investors who understand this balance will be better positioned to capture the value that private credit can deliver in the years ahead.

Conclusion

Private credit has emerged as one of the most dynamic and influential forces in global finance. What began as a niche strategy in the years following the financial crisis has grown into a multitrillion dollar ecosystem that now shapes how companies borrow, how investors seek yield, and how markets allocate capital. Its rise reflects a combination of structural changes, including tighter banking regulation, the growing influence of private markets, and the increasing demand for income focused investment solutions.

In a high rate environment, private credit stands out as a rare winner. Floating rate structures, strong covenant protections, and an illiquidity premium have allowed private lenders to generate attractive returns even as traditional fixed income struggles with duration risk and volatile market pricing. Borrowers have embraced private lenders for their speed, flexibility, and ability to design tailored solutions that banks often cannot provide. Investors, in turn, have recognized the value of stable income in an uncertain world.

Yet the growth of private credit brings important responsibilities. The asset class carries inherent risks, including credit deterioration in weaker economic periods, limited liquidity, and the challenge of navigating opaque valuations. The increasing size of the industry may also lead to greater regulatory attention. These factors require investors to approach private credit with discipline, a long term perspective, and a clear understanding of both its strengths and its vulnerabilities.

Looking ahead, private credit is positioned to remain a powerful force in global finance. Demographic changes, evolving regulation, technological innovation, and the globalization of alternative lending all point toward continued expansion. The industry is entering a new phase marked by greater sophistication, deeper integration with private equity, and a broadening range of strategies that extend beyond traditional direct lending.

For investors willing to embrace its complexities, private credit offers a compelling combination of yield, resilience, and strategic relevance. Its ascent reflects a fundamental shift in how modern financial systems function. In a world defined by higher rates, tighter liquidity, and increasing uncertainty, private credit has become not only the new king of yield but also a central pillar in the future of global capital markets.